Knoxville, Tennessee, July 27, 2020 – Mountain Commerce Bancorp, Inc. (the “Company”) (OTCQX: MCBI), the holding company for Mountain Commerce Bank (the “Bank”), today announced earnings and related data as of and for the three and six months ended June 30, 2020.

Highlights

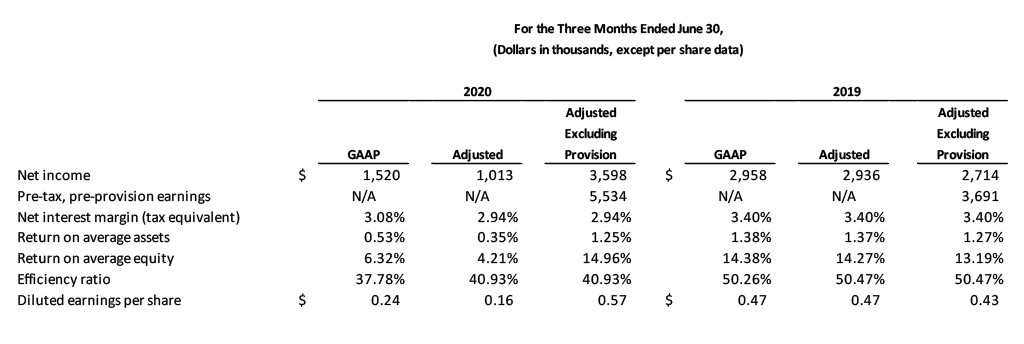

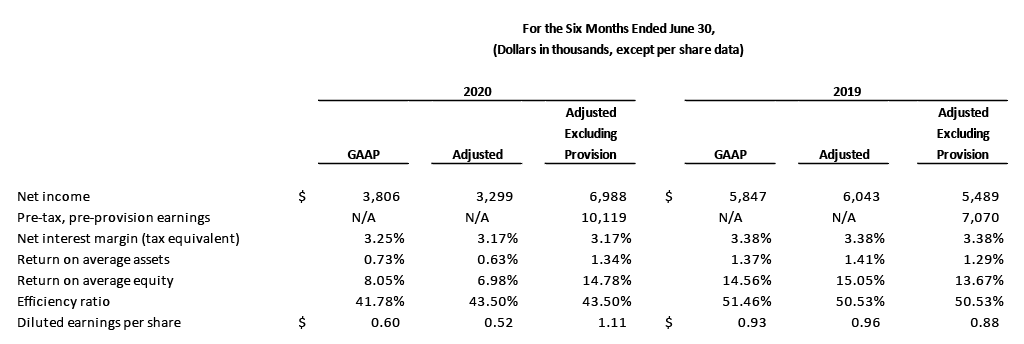

The following tables highlight the trends that the Company believes are most relevant to understanding the performance of the Company. As further detailed in Appendix A to this press release, (i) adjusted results (which are non-GAAP financial measures) reflect adjustments for investment gains and losses and the impact of PPP fee amortization, net of costs and (ii) adjusted results excluding provision for loan losses (which are also non-GAAP financial measures. See Appendix B to this press release for more information on our tax equivalent net interest margin.

Management Commentary

William E. “Bill” Edwards, III, President and Chief Executive Officer of the Company, commented, “We are pleased with our second quarter results which continued to be strong with our adjusted net income excluding the provision for loan losses increasing 33% from $2.7 million in the second quarter of 2019 to $3.6 million in the same quarter of 2020. As a result of the continuing economic downturn, we adjusted several components of our allowance for loan losses model, which contributed to an additional $3.5 million of reserves in the second quarter of 2020, bringing our allowance to non-PPP loans to 1.30%. During these uncertain times, we believe it is particularly important to operate efficiently, which is reflected in our adjusted efficiency ratio dropping below 41% this quarter. The Company has also been a significant participant in the Paycheck Protection Program (PPP), funding 765 loans for over $107 million in principal amount and generating fee income of nearly $3.5 million, which will be recognized over the life of the PPP loans. The Company recently announced that it successfully raised $10 million of subordinated debt in a private offering to institutional accredited investors. This offering closed on July 15, 2020. While we are currently well capitalized, the subordinated debt will provide an additional source of strength and capital for the Bank should our borrowers be more negatively impacted by the economic disruption associated with COVID-19 than we currently anticipate. Finally, as we look ahead, we intend to look for opportunities to grow our franchise, while staying focused on what we do best – relationship banking.”

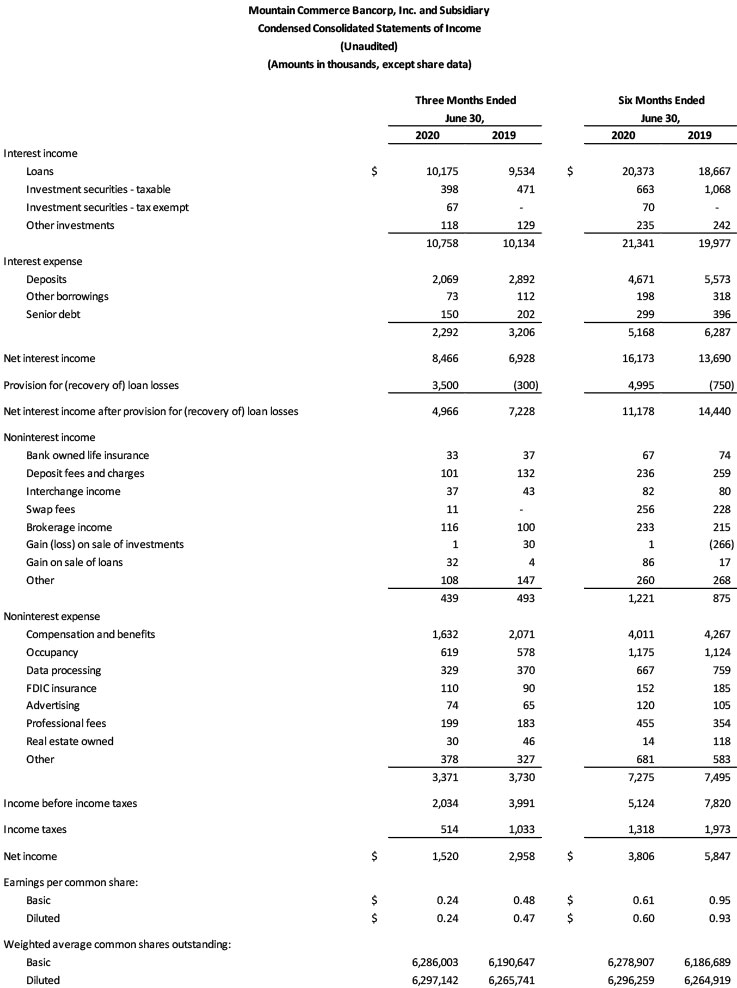

Net Interest Income

Net interest income increased $1.5 million, or 22.2%, from $6.9 million for the three months ended June 30, 2019 to $8.5 million for the same period in 2020. The increase between the periods was primarily the result of the following factors:

- Average interest-earning assets grew $290.9 million, or 35.6%, from $817.5 million to $1.108 billion, due in part to PPP loans.

- Average net interest-earning assets grew $106.6 million, or 65.1%, from $163.8 million to $270.4 million, funded by increases in noninterest bearing deposits and Federal Home Loan Bank (FHLB) / Federal Reserve Bank (FRB) borrowings.

These increases were partially offset by a decrease in net interest margin from 3.40% for the three months ended June 30, 2019 to 3.08% for the same period of 2020 as a result of increased liquidity and a decrease in the yield on interest-earning assets from 4.92% during the three months ended June 30, 2019 to 3.91% during the same period in 2020 due to lower yields on PPP loans, offset in part by lower funding costs.

Net interest income increased approximately $2.5 million, or 18.1%, from $13.7 million for the six months ended June 30, 2019 to $16.1 million for the same period in 2020. The increase between the periods was primarily the result of the following factors:

- Average interest-earning assets grew $186.1 million, or 22.8%, from $816.1 million to $1.002 billion.

- Average net interest-earning assets grew $78.9 million, or 51.6%, from $152.9 million to $231.8 million, funded by increases in noninterest bearing deposits and FHLB / FRB borrowings.

These increases were partially offset by a decrease in net interest margin from 3.38% for the six months ended June 30, 2019 to 3.25% during the same period of 2020 as a result of increased liquidity and a decrease in the yield on interest-earning assets from 4.94% during the six months ended June 30, 2019 to 4.29% during the same period in 2020 due to lower yields on PPP loans, offset in part by lower funding costs.

The Company recognized approximately $0.4 million of net PPP loan origination fees through net interest income during the three and six months ended June 30, 2020.

Provision For Loan Losses

A provision for loan losses of $3.5 million and $5.0 million was recorded for the three and six months ended June 30, 2020, respectively, as a result of the Company increasing the qualitative factors in its allowance for loan loss model and increasing reserve factors on certain loans to borrowers more likely to be impacted by the COVID-19 pandemic. A recovery of loan losses of $0.3 million and $0.8 million was recorded in the three and six months ended June 30, 2019, respectively.

Noninterest Income

Noninterest income decreased $0.1 million, or 11.0%, from $0.5 million in the second quarter of 2019 to $0.4 million in the same quarter of 2020. The decrease was primarily due to modest declines in deposit fees and charges and gains on the sale of investments.

Noninterest income increased $0.3 million, or 39.5%, from $0.9 million during the six months ended June 30, 2019 to $1.2 million during the same period of 2020. The increase was primarily due to a loss on the sale of investments of $0.3 million during the six months ended June 30, 2019 and an increase in the gain on sale of loans during the six months ended June 30, 2020.

Noninterest Expense

Noninterest expense decreased approximately $0.4 million, or 9.6%, from $3.7 million in the second quarter of 2019 to $3.4 million in the second quarter of 2020. This decrease was primarily the result of a decline in compensation and benefits expense of $0.3 million due to deferred loan origination costs on PPP loans.

Noninterest expense decreased $0.2 million, or 2.9%, from $7.5 million for the six months ended June 30, 2019 to $7.3 million for the same period of 2020. This decrease was primarily the result of declines in compensation and benefits resulting from deferred loan origination costs on PPP loans, and residual data processing and real estate owned expenses, offset partially by increases in professional fees.

Income Taxes

The effective tax rate of the Company was 25.3% and 25.9% for the three months ended June 30, 2020 and 2019, respectively. The effective tax rate of the Company was 25.7% and 25.2% for the six months ended June 30, 2020 and 2019, respectively. The Company’s marginal tax rate of 26.14% is favorably impacted by certain sources of non-taxable income including BOLI and investments in municipal securities.

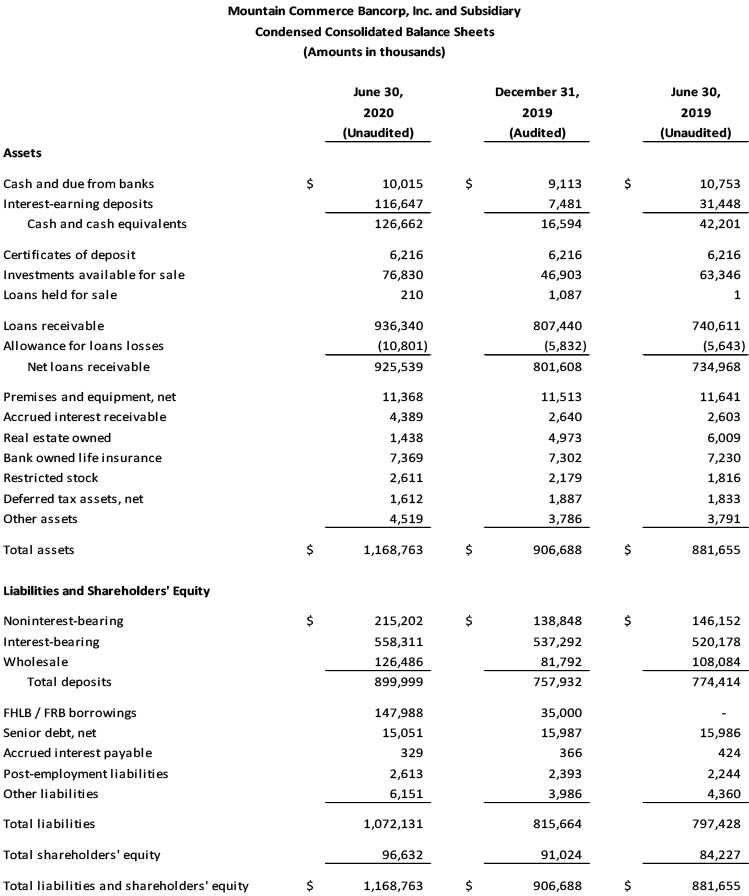

Balance Sheet

Total assets increased $262.1 million, or 28.9%, from $906.7 million at December 31, 2019 to $1.169 billion at June 30, 2020. The increase was primarily driven by the following factors:

- Interest-earning deposits increased $109.2 million from $7.5 million at December 31, 2019 to $116.7 million at June 30, 2020. The increase was driven primarily by higher noninterest-bearing deposit balances resulting from PPP lending balances that remained on deposit at the Company as well as a general increase in customer deposit balances. The Company believes it is prudent to maintain higher levels of liquidity during the economic downturn.

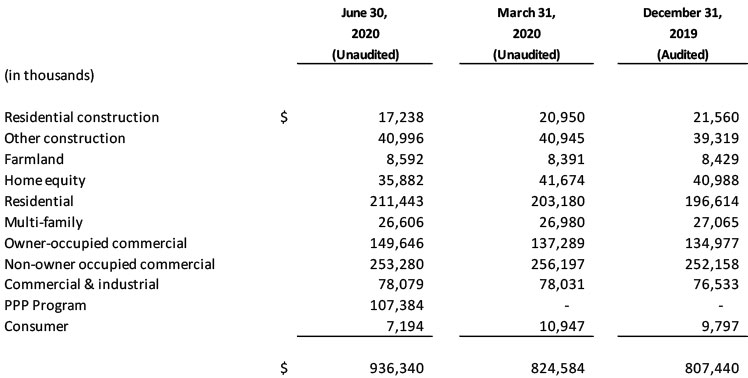

- Loans receivable increased $128.9 million, or 16.0%, from $807.4 million at December 31, 2019 to $936.3 million at June 30, 2019. $107.4 million of this increase resulted from PPP loans.

The following summarizes changes in loan balances over the last three quarters:

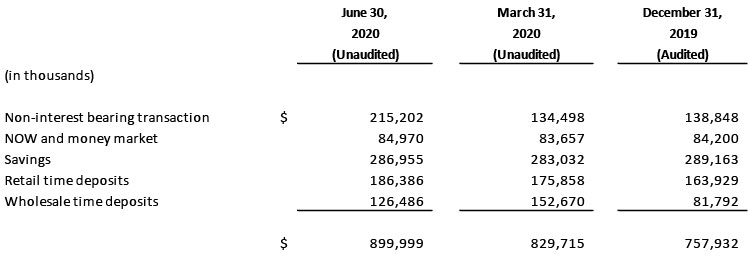

Total deposits increased $142.1 million, or 18.7%, from $757.9 million at December 31, 2019 to $900.0 million at June 30, 2020. In addition to the increase in noninterest-bearing deposit balances resulting principally from the PPP program, wholesale deposit balances increased $44.7 million, or 54.6%, from December 31, 2019 to June 30, 2020 due to the Company’s decision to maintain higher levels of liquidity during the economic downturn.

The following summarizes changes in deposit balances over the last three quarters:

FHLB / FRB borrowings increased $113.0 million, or 322.8%, from $35.0 million at December 31, 2019 to $148.0 million at June 30, 2020. $98.0 million of this increase related to borrowings from the FRB to fund PPP loans.

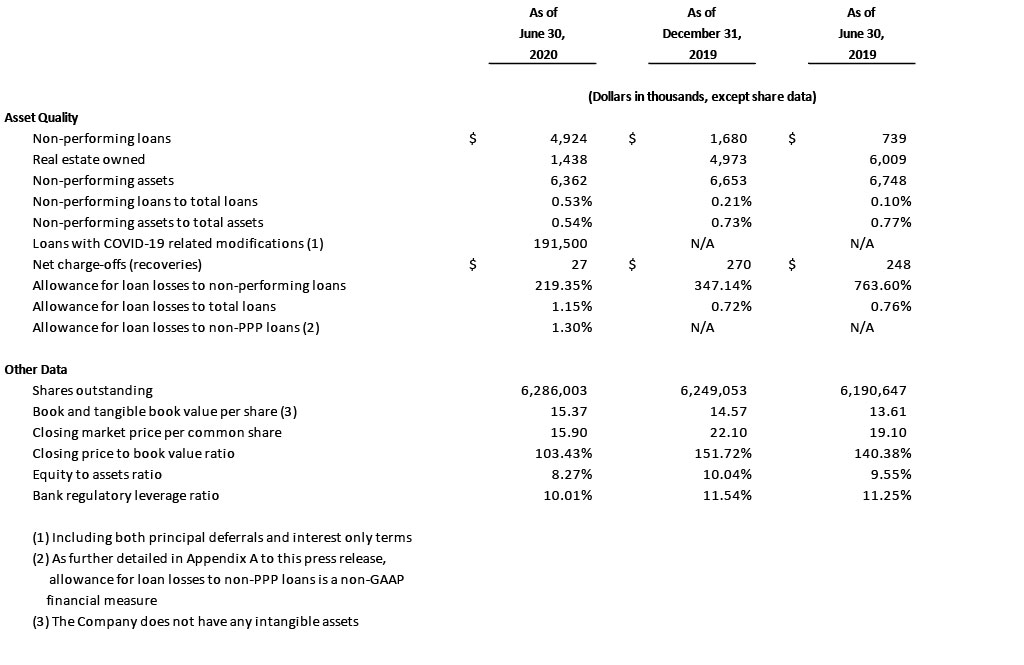

Total equity increased $5.6 million, or 6.1%, from $91.0 million at December 31, 2019 to $96.6 million at June 30, 2020. This increase was primarily comprised of net income of $3.8 million and net improvement in the fair value of the Company’s investments and derivatives of $1.6 million. Tangible book value per share improved from $14.57 at December 31, 2019 to $15.37 at June 30, 2020. Equity to assets declined from 10.04% at December 31, 2019 to 8.27% at June 30, 2020 because of the meaningful increase in total assets, including the PPP loans.

Asset Quality

Non-performing loans to total loans increased from 0.21% at December 31, 2019 to 0.53% at June 30, 2020. The increase was due to the addition of 2 real estate secured relationships for which no loss is currently expected. Non-performing assets to total assets decreased from 0.73% at December 31, 2019 to 0.54% at June 30, 2020, primarily as a result of the sale of several real estate owned properties. Net charge-offs of $27 thousand were recognized during the first six months of 2020. The allowance for loan losses to total loans (excluding PPP loans) increased from 0.72% at December 31, 2019 to 1.30% at June 30, 2020 and coverage of non-performing loans remains strong at 219.35% at June 30, 2020.

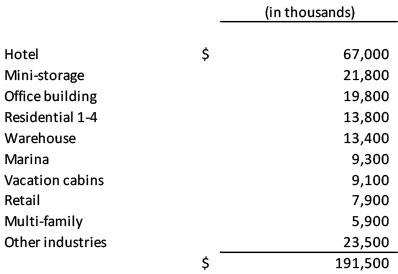

The Company had granted principal and/or interest deferrals on loans totaling $191.5 million in aggregate principal amount, or approximately 23% of its non-PPP loan portfolio, in response to COVID-19 as of June 30, 2020. These deferrals were to customers in the following industries:

Other industries not detailed in the table above including restaurants, automobile, medical, entertainment, and others were individually below $5 million of exposure. Approximately 57% of the deferrals involved principal, while 43% involved an interest only period.

Non-GAAP Financial Measures

Statements included in this press release include non-GAAP financial measures and should be read along with the accompanying tables in Appendix A, which provide a reconciliation of these non-GAAP financial measures to the most directly comparable GAAP financial measures. This press release and the accompanying tables discuss financial measures such as adjusted net income, adjusted diluted earnings per share, adjusted return on average assets, adjusted return on average equity, adjusted net interest margin, and adjusted efficiency ratio, both including and excluding the provision for (recovery of) loan losses, which are all non-GAAP financial measures. We also present in this press release and the accompanying tables the allowance for loan losses to loans excluding PPP loans which is also a non-GAAP financial measure. We believe that such non-GAAP financial measures are useful because they enhance the ability of investors and management to evaluate and compare the Company’s operating results from period to period in a meaningful manner. Non-GAAP financial measures should not be considered as an alternative to any measure of performance calculated pursuant to GAAP, nor are they necessarily comparable to non-GAAP financial measures that may be presented by other companies. Investors should consider the Company’s performance and financial condition as reported under GAAP and all other relevant information when assessing the performance or financial condition of the Company. Non-GAAP financial measures have limitations as analytical tools, and investors should not consider them in isolation or as a substitute for analysis of the Company’s results or financial condition as reported under GAAP.

Forward-Looking Statements

This press release contains forward-looking statements. The words “expect,” “intend,” “should,” “may,” “could,” “believe,” “suspect,” “anticipate,” “seek,” “plan,” “estimate” and similar expressions are intended to identify such forward-looking statements, but other statements not based on historical fact may also be considered forward-looking. Such forward-looking statements involve known and unknown risks and uncertainties that include, without limitation, (i) further deterioration in the financial condition of our borrowers resulting in significant increases in loan losses and provisions for those losses, (ii) the effects of the emergence of widespread health emergencies or pandemics, including the magnitude and duration of the COVID-19 pandemic and its impact on general economic and financial market conditions and on our and our customers’ business, results of operations, asset quality and financial condition; (iii) deterioration in the real estate market conditions in our market areas, (iv) the impact of increased competition with other financial institutions, including pricing pressures, and the resulting impact our results, including as a result of compression to our net interest margin, (v) the further deterioration of the economy in our market areas, (vi) fluctuations or differences in interest rates on loans or deposits from those that we are modeling or anticipating, including as a result of our inability to better match deposit rates with the changes in the short-term rate environment, or that affect the yield curve, (vii) the ability to grow and retain low-cost core deposits, (viii) significant downturns in the business of one or more large customers, (ix) our inability to maintain the historical growth rate of our loan portfolio, (x) risks of expansion into new geographic or product markets, (xi) the possibility of increased compliance and operational costs as a result of increased regulatory oversight, (xii) our inability to comply with regulatory capital requirements, including those resulting from changes to capital calculation methodologies and required capital maintenance levels, (xiii) changes in state or Federal regulations, policies, or legislation applicable to banks and other financial service providers, including regulatory or legislative developments arising out of current unsettled conditions in the economy, (xiv) changes in capital levels and loan underwriting, credit review or loss reserve policies associated with economic conditions, examination conclusions, or regulatory developments, (xv) inadequate allowance for loan losses, (xvi) results of regulatory examinations, (xvii) the vulnerability of our network and online banking portals, and the systems of parties with whom we contract, to unauthorized access, computer viruses, phishing schemes, spam attacks, human error, natural disasters, power loss and other security breaches, (xviii) the possibility of additional increases to compliance costs as a result of increased regulatory oversight, (xix) loss of key personnel, and (xx) adverse results (including costs, fines, reputational harm and/or other negative effects) from current or future obligatory litigation, examinations or other legal and/or regulatory actions. These risks and uncertainties may cause our actual results or performance to be materially different from any future results or performance expressed or implied by such forward-looking statements. Our future operating results depend on a number of factors which were derived utilizing numerous assumptions that could cause actual results to differ materially from those projected in forward-looking statements.

About Mountain Commerce Bancorp, Inc. and Mountain Commerce Bank

Mountain Commerce Bancorp, Inc. is the holding company of Mountain Commerce Bank. The Company’s shares of common stock trade on the OTCQX under the symbol “MCBI”.

Mountain Commerce Bank is state-chartered financial institution that traces its history over a century and is headquartered in Knoxville, Tennessee serving East Tennessee through 5 branches located in Erwin, Johnson City, Knoxville and Unicoi. The Bank focuses on relationship banking of small and medium-sized businesses and high net worth individuals who value the personal service and attention that only a community bank can offer. For further information, please visit us at www.mcb.com